Whereas COVID was raging, the bounce in home costs and a rising inventory market have been dramatically enhancing U.S. employees’ retirement funds.

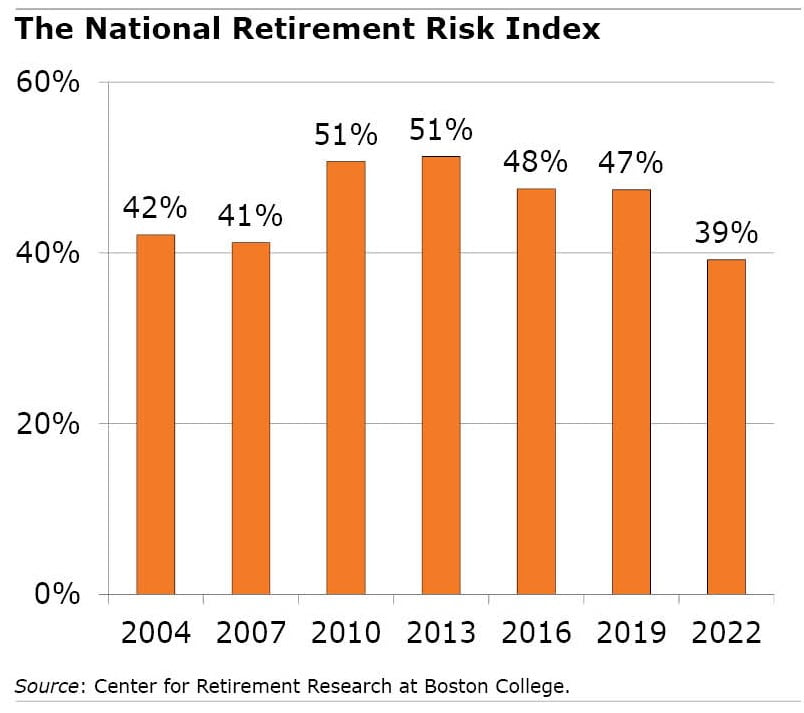

In 2022, the share of households that weren’t saving sufficient to keep up their way of life after they retire dropped to 39 p.c, from 47 p.c in 2019, in response to the Middle for Retirement Analysis, which sponsors this weblog.

That 39 p.c is the bottom stage within the almost 20 years the middle has been analyzing the info within the Federal Reserve Board’s Survey of Client Funds, which is carried out each three years.

However the information just isn’t fairly nearly as good because it seems, as a result of the rise in home costs in 2020 by means of 2022, which continues at this time, was the most important single motive for the advance.

Sure, Individuals are wealthier on paper, because of a mixture of previous mortgages with low rates of interest and rising home costs fueled by sturdy housing demand throughout COVID in suburban and rural markets. Among the many narrower group of people that personal their properties, the share of households in danger dropped sharply, from 34 p.c to 24 p.c.

However it’s also pretty uncommon for retirees to capitalize on their housing wealth by changing it into revenue by downsizing to a cheaper house or taking out a reverse mortgage. A conversion by means of a reverse mortgage is a core assumption within the middle’s evaluation. In 2022, solely 64,437 householders took out the federally insured reverse mortgage that turns into an choice at age 62.

The rise in house costs wasn’t the one factor boosting retirement wealth, nonetheless. A rising inventory market was the second most necessary motive for the improved outlook.

The Customary & Poor’s 500 inventory index – regardless of the 2022 market droop – gained greater than 20 p.c after inflation throughout the three-year interval. These good points primarily benefited the rich, the place inventory possession is concentrated – in addition they are likely to personal their properties.

However funding portfolios additionally grew for lower- and middle-income employees who’re saving in an employer’s 401(okay)-style retirement plan. Amongst households with a 401(okay), the share at-risk fell from 42 p.c to 35 p.c.

Decrease- and middle-income employees additionally padded their financial savings accounts when Congress supplied a beneficiant package deal of economic help to assist them deal with the financial slowdown within the first yr of the pandemic.

The development in Individuals’ retirement funds is encouraging. However even this conservative estimate that counts little-used house fairness as retirement wealth leaves 4 out of ten households with the opportunity of a drop of their way of life as soon as they retire.

This, the researchers conclude, “verify[s] that we have to repair our retirement system in order that Social Safety is financially sound and employer plan protection is common.”

Squared Away author Kim Blanton invitations you to comply with us @SquaredAwayBC on X, previously generally known as Twitter. To remain present on our weblog, be a part of our free e mail record. You’ll obtain only one e mail every week – with hyperlinks to the 2 new posts for that week – if you enroll right here. This weblog is supported by the Middle for Retirement Analysis at Boston Faculty.